Shopping for a lakefront or ranch estate in Horseshoe Bay and noticing prices that climb well above typical mortgage limits? You are not alone. Many luxury homes around Lake LBJ sit beyond standard conforming ranges, which means you will likely use a jumbo loan. In this guide, you will learn what counts as a jumbo in Llano County, what lenders look for, which documents to gather, and how unique property features like waterfront access or barns can affect the process. Let’s dive in.

What counts as a jumbo in Horseshoe Bay

A mortgage becomes a jumbo when the loan amount is higher than the conforming limit set each year. For 2024, the national baseline conforming limit for a single-family home is $766,550, according to the FHFA’s conforming loan limits. Llano County follows this baseline, so any loan above that figure is jumbo.

Here is a simple example. If you buy a $1,000,000 home with 20 percent down, your loan would be $800,000. Because $800,000 is above $766,550, the loan is jumbo. In Horseshoe Bay, many luxury lakefront and custom homes cross this threshold.

Jumbo loans are not purchased by Fannie Mae or Freddie Mac, so lenders set stricter standards to manage risk. That is why you will see higher credit expectations, tighter debt limits, and larger reserve requirements.

How jumbo lenders evaluate you

Credit score and DTI

Most jumbo programs price best for strong credit. Many lenders look for scores in the mid 700s, often 720 or higher. Some may accept lower scores, but you will usually see a higher rate and tighter rules.

Debt-to-income ratios also matter. Many jumbo programs target a DTI at or below 43 to 45 percent for a primary residence. If your profile shows strong compensating factors like a lower loan-to-value, very high credit, or large cash reserves, a lender may allow a little more flexibility.

Down payment and LTV

Your down payment drives loan-to-value, which is a big pricing factor. Typical ranges many buyers see:

- Primary residence: up to 80 to 90 percent LTV with select programs, but 80 percent or less often gets better pricing.

- Second homes: usually 80 percent LTV max. Plan for at least 20 percent down.

- Investment properties: often 70 to 75 percent LTV caps with stricter terms.

A larger down payment lowers risk and can help offset other weak spots in your profile.

Cash reserves

Jumbo loans commonly require liquid reserves equal to months of total housing payments. Expect:

- Primary residence: about 6 to 12 months of PITI.

- Second home: often 12 to 24 months of PITI.

- Investment property: commonly 12 to 24 months of PITI.

If you are self-employed or using a higher LTV, the reserve ask may increase.

Rate drivers you can control

Your rate depends on several items: credit score, LTV, occupancy type, loan amount, loan term, and whether the lender plans to keep the loan on its books. Market conditions also matter. While you cannot control the market, you can shape your profile with a stronger down payment, better credit hygiene, and by choosing a loan term that fits your timeline.

If you want an overview of how lenders think about mortgages and underwriting basics, the CFPB’s mortgage resources are a helpful primer.

Documents to prepare early

Full-documentation is the norm for competitive jumbo pricing. You can save time by gathering these items upfront:

- Last 2 years of personal federal tax returns; business returns if self-employed.

- Last 2 years of W-2s for employed borrowers and recent pay stubs covering 30 to 60 days.

- Bank and investment statements for the past 2 to 3 months to verify assets and reserves.

- Signed tax returns and authorization for IRS transcripts.

- Statements for retirement and brokerage accounts used for down payment or reserves.

- Gift letter and source documentation if using gift funds, if allowed by the program.

- Photo ID and explanations for any large deposits.

Alternative documentation programs exist, such as bank-statement or asset-depletion loans, but they usually come with higher rates and lower maximum LTVs.

Primary, second home, or investment

Your intended use affects terms and underwriting:

- Primary residence: Generally the most flexible. You may find higher LTV options and lighter reserve requirements compared with other uses.

- Second home: Common around Lake LBJ. Plan for at least 20 percent down and stronger reserves. Lenders will verify it is truly a second home.

- Investment property: Tighter terms, lower LTVs, and higher reserves. Income from the property may be considered, but guidelines vary by lender.

If you are buying a second home that could also serve as a rental, clarify your intended use with your lender before you write an offer.

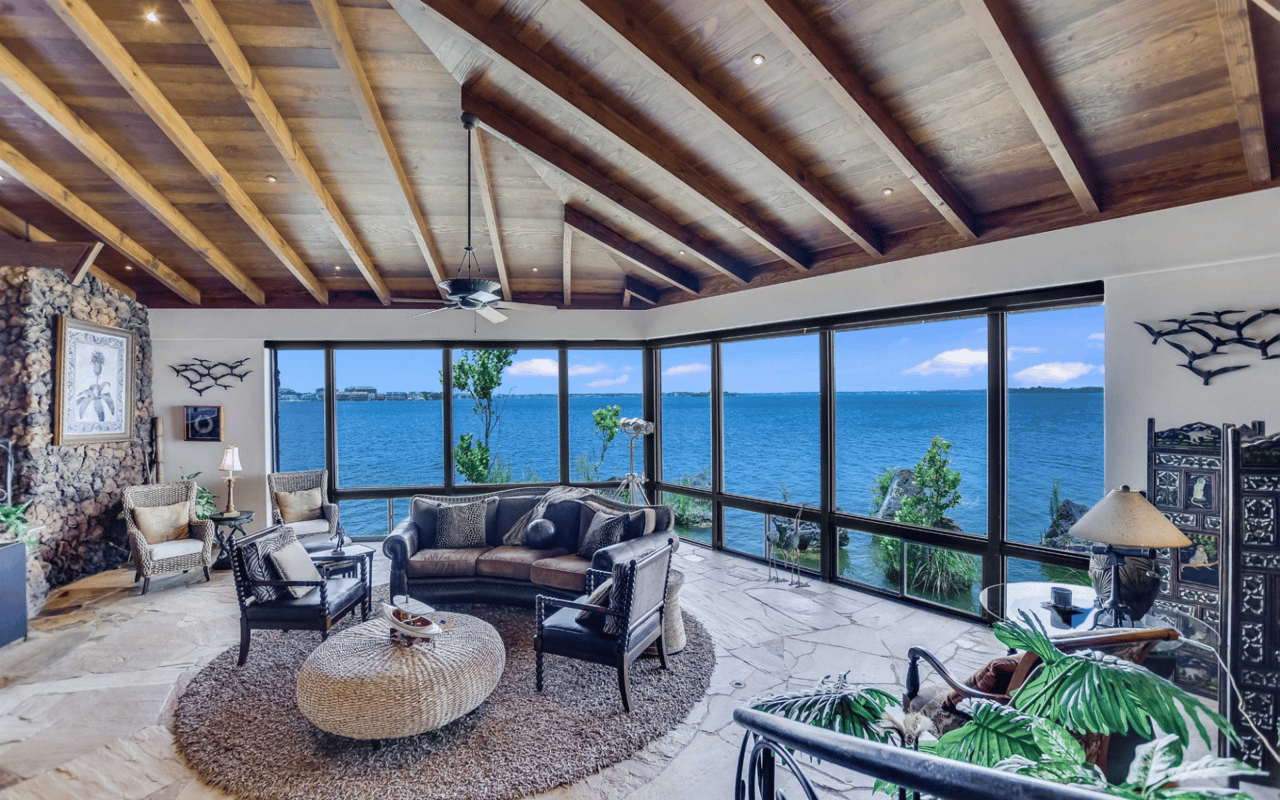

Property factors unique to Horseshoe Bay

Appraisals for unique homes and ranches

Waterfront residences, custom estates, equestrian properties, and acreage tracts do not always have many direct comparable sales. Appraisers may use more distant comps or lean on the cost approach. Expect longer appraisal timelines and higher appraisal fees for complex properties.

If your home includes barns, arenas, boathouses, or accessory dwellings, a lender may request extra detail in the report. Planning for a longer appraisal window can protect your rate lock and closing date.

Resort HOAs and warrantability

Many Horseshoe Bay properties sit in gated or resort-style communities with HOAs. Lenders review HOA financials, owner-occupancy ratios, and any active litigation. Some programs limit loans in non-warrantable communities or certain condo projects. Ask your lender how they will evaluate the community before you waive contingencies.

Flood and insurance readiness

Lakefront or lakeside homes may lie within FEMA special flood hazard areas. If your parcel is in a mapped flood zone, your lender will require flood insurance. You can confirm your parcel’s status using the FEMA Flood Map Service Center.

Even if flood insurance is not required, consider a quote to manage risk. For high-value homes, review replacement-cost coverage early, since insurers sometimes limit coverage amounts on unique waterfront or ranch properties.

Wells, septic, and utilities

Rural and semi-rural properties around Horseshoe Bay often use private wells and septic systems. Lenders may ask for inspections showing that systems function properly. If a report lists a needed repair, the appraiser could factor that into value or the lender could require the fix prior to closing.

Title, mineral rights, and easements

In Texas, mineral rights and easements can affect land use and value. Your title commitment will outline existing easements and any reservations. For properties with agricultural exemptions, understand how your use will maintain or change that status and what it means for ongoing tax costs.

Example jumbo scenarios

- $1,000,000 lake house with 20 percent down: The loan would be $800,000, which is jumbo. A well-qualified buyer might target a DTI under 43 percent, a credit score around 720 or higher, and reserves of 6 to 12 months PITI for a primary residence or closer to 12 months for a second home.

- $1,500,000 custom estate with 30 percent down: The loan would be $1,050,000. The lower 70 percent LTV can improve pricing and may offset a higher DTI or a more complex income profile. Expect an in-depth appraisal and potentially longer due diligence for unique improvements.

These examples do not replace lender advice, but they show how down payment and occupancy shape the offer you can accept and the timeline you should plan for.

Timeline and locking strategy

Complex appraisals and HOA reviews can extend the closing timeline. Discuss a rate-lock period that covers appraisals and underwriting with room for the unexpected. For unique property types, a 45 to 60 day lock can be a smart starting point. Ordering the appraisal early, confirming insurance availability, and completing title and flood reviews upfront can help you close on time.

If you are self-employed or using alternative documentation, add time for income analysis. Provide clean, complete documentation at the start of underwriting to avoid extension fees and lock re-pricing.

Plan your purchase with a local guide

Buying a luxury home in Horseshoe Bay is as much about place as it is about financing. You deserve a team that understands lakefront regulations, resort communities, acreage nuances, and seasonal market rhythms. With five decades in the Highland Lakes and Hill Country, LandMasters pairs local insight with a calm, organized buying experience so you can plan your jumbo financing and property due diligence with confidence.

When you are ready to explore lakefront, ranch, or resort homes, reach out to Landmasters Real Estate. We will help you navigate the local market, coordinate key steps with your lender and title company, and move from offer to closing with clarity.

FAQs

What is a jumbo loan in Horseshoe Bay for 2024?

- Any mortgage amount above the FHFA’s 2024 conforming limit of $766,550 for a single-family home is considered jumbo in Llano County.

How much down payment do I need for a jumbo on a lake house?

- Plan for at least 20 percent down for many programs, with some primary-home options going higher or lower depending on your profile and lender.

What credit score and reserves are typical for jumbo financing?

- Many lenders price best around 720-plus credit, with reserves of 6 to 12 months PITI for primary homes and 12 to 24 months for second homes or investments.

Do appraisals take longer for waterfront or horse properties near Lake LBJ?

- Often yes, because comparable sales are limited and unique improvements require more analysis, which can increase timeline and appraisal fees.

Is flood insurance required for a Lake LBJ waterfront home?

- If the home is in a FEMA special flood hazard area, lenders will require flood insurance; check the FEMA Flood Map Service Center to confirm your parcel.

Can I qualify for a jumbo if I have high assets but irregular income?

- Some lenders offer bank-statement or asset-based jumbo programs, but they usually come with higher rates and lower maximum LTVs than standard full-doc loans.